GAD Release 8th Edition of the Ogden Tables

21/07/2020

On Friday, 17 July 2020, the Government Actuary Department (GAD) released the 8th Edition of the actuarial tables for use in personal injury and fatal accident cases, known as the Ogden Tables. There were a number of additions and changes made by the Ogden Working Party, which are well documented within the opening sections, however the most noticeable change is the mortality assumptions, which has led to a blanket reduction in life and pension multipliers.

Multipliers published in the 7th edition of the Ogden Tables were calculated using mortality rates from the 2008-based projections; the 8th edition provides multipliers based on mortality rates from the most recent, 2018-based, projections (published at the end of 2019).

The mortality assumptions are based on average or typical life expectancy for males and females relating to the general population of the United Kingdom as a whole. As such it would need to be evidenced if life expectancy was “atypical” in an individual case and can be expected to experience a significantly shorter or longer than average lifespan, to an extent greater than would be encompassed by reasonable variations resulting from place of residence, lifestyle, educational level, occupation and general health status.

Contrary to previous indications, the expectations of life in Ogden 8 are lower than in the 7th edition. The working party believe this reflects both the lower decreases in mortality than previously projected between 2008 and 2018 and more pessimistic assumptions adopted by the ONS regarding the future rates of improvement of mortality at some ages over the next few years, but especially at older ages.

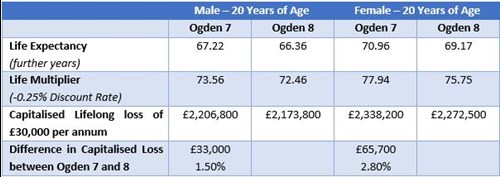

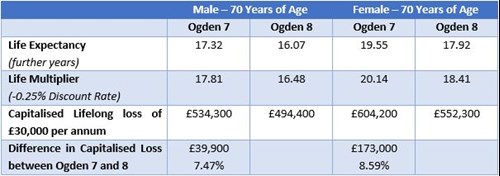

As a result, the life multipliers have reduced for all in comparison to Ogden 7, with a bigger impact on those of an older age, the effect being as much as a 9% reduction in quantified damages, as illustrated in Fig 2.

Fig. 1

Fig. 2

For those who have suffered lifelong recurring need or loss of significant value, such as care and case management, the effect of the new mortality data could be detrimental to their future financial needs if the mortality risk is not considered at the outset. It is therefore our view that in all cases where there is a significant recurring loss which is incurred for life, or a substantial period of time, then Periodical Payments should at least be considered, if only to be discounted prior to settlement negotiations.

We can provide reports detailing the factors to consider and analysis of the potential mortality risk and investment risk involved with each form of award depending on the Claimant’s individual circumstances.

For further information please contact us at enquiries@adroitfp.co.uk.